Global vegetable oil prices increased in June, according to the benchmark United Nations’ Food and Agriculture Organization (FAO) Vegetable Oil Price Index released on 3 July.

The increase reflected the combined effect of higher palm and rapeseed oil prices and stable sunflower oil prices, which more than offset lower soyabean oil quotations.

“Following a brief decline in May, international palm oil prices rebounded in June, supported mainly by expectations of tighter export availability from Indonesia, on account of stronger domestic feedstock demand for biodiesel and potentially lower output due to declining yields,” the FAO said.

“Global rapeseed oil prices continued to rise, driven largely by firm biofuel demand and unfavourable weather conditions affecting plantings in Australia and Canada.”

World sunflower oil prices remained broadly stable, as the impact of continued tightness in 2025/26 was offset by expectations of increased supplies in 2026/27.

Meanwhile, global soyabean oil quotations declined slightly, under pressure from seasonally increasing supplies in South America and declining crude oil prices.

The FAO’s vegetable oil price index illustrates the changes in international prices of the 10 most important vegetable oils in world trade, weighted according to their export shares.

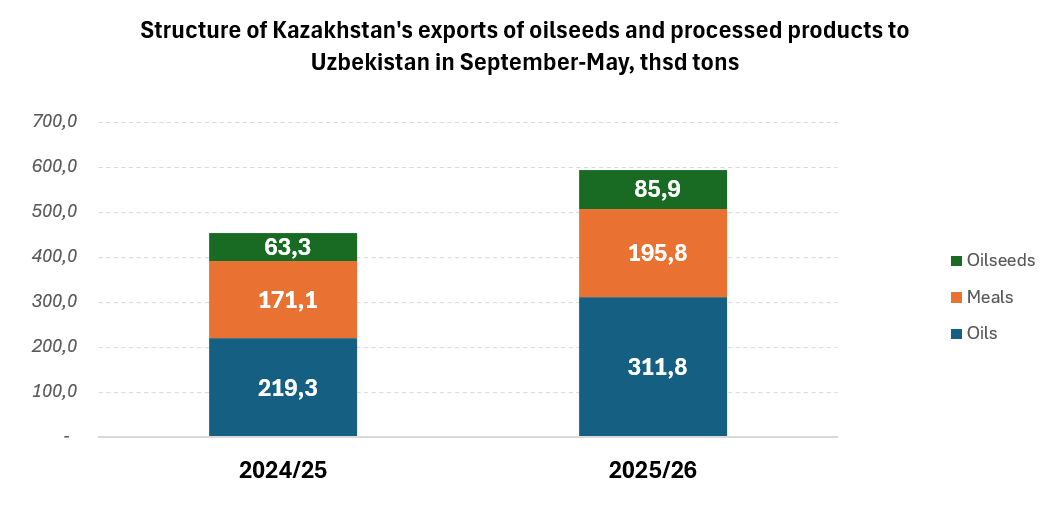

Uzbekistan remains one of the key buyers of Kazakh oilseed products and continues to increase imports. According to APK-Inform, citing official statistics, vegetable oils and meals account for the largest share of supplies.

Uzbekistan imported about 312,000 tons of vegetable oils, up 42% from the same period of the previous season.

Sunflower oil accounted for the largest share, with shipments reaching about 293,000 tons, up 38% from the previous season. Over the past two seasons, this product has accounted for nearly 50% of Kazakhstan's total oilseed exports to Uzbekistan.

Sunflower meal/cake ranked second, with shipments to Uzbekistan reaching 156,000 tons in September-May of the 2025/26 MY, up 7% from the previous season.

Shipments of rapeseed meal/cake also increased significantly, rising 92% to nearly...

Beijing’s commitments to purchase US soyabeans has led to a modest increase in American sales to China, CNBC reports.

US soyabean sales to China – the world’s largest importer of the oilseed – had plunged amid recent trade tensions between the two countries and Beijing had diversified its sourcing to Brazil and Argentina in a bid to ensure food security, the 23 June report said.

According to CNBC analysis of Chinese customs data accessed through Wind Information, although the USA and Brazil each accounted for around 40% of China’s soyabean imports a decade ago, the South American country started to take a far larger share in 2018 after the first round of US tariffs on China.

As of the first five months of 2026, more than 60% of Chinese soyabean imports came from Brazil, 23% from the USA and 10% from Argentina, the data showed.

According to official US figures, the value of American soyabean exports to China plunged by 76% last year to US$3.1bn, down sharply from a peak of US$17.9bn in 2022.

Despite this, at 7.37M tonnes, US soyabeans remained the largest American agricultural export to China during the last calendar year.

In May, following US President Donald Trump’s meeting with Chinese President Xi Jinping in Beijing, the White House said China would buy agricultural commodities worth at least US$17bn/year through to 2028.

That amount would be “in addition to the soyabean purchase commitments it [China] made in October 2025”, CNBC reported at the time.

In a previous meeting between Trump and Xi last year, the USA said China had agreed to purchase 12M tonnes of US soyabeans in the marketing year ending August 2026 and at least 25M tonnes/year of American soyabeans over the following three marketing years.

China had bought all 12M tonnes of US soyabeans that it had agreed to purchase up to August 2026 with the bulk of that volume shipped, Jim Sutter, CEO of the US Soybean Export Council told CNBC.

Purchases of the subsequent 25M tonnes had begun in the week before the report, he added.

BRUSSELS, BELGIUM — A coalition of European and international organizations representing the oilseeds industry welcomed a vote by the European Parliament rejecting a proposal that would have classified soybean oil as a high indirect land-use change (ILUC) risk feedstock under the Renewable Energy Directive.

The organizations said in a joint statement that the July 8 outcome — the adoption of a motion for a resolution objecting to Commission Delegated Regulation (EU) 2026/2680 — was an important step toward safeguarding the competitiveness and resilience of the European soy value chain. To enter into force, the delegated regulation would have had to be approved by both the European Council and the European Parliament.

“This vote sends a strong signal in favor of evidence-based policymaking and greater coherence between the EU’s renewable energy, agriculture and food security objectives,” the coalition said. “It safeguards the competitiveness of the European soy value chain, protects farmers and processors, and supports the EU’s ambition to strengthen domestic protein production and strategic autonomy.”

The coalition thanked parliament for recognizing the strategic importance of soybeans for Europe’s food and feed supply and for rejecting a methodology that they said would have undermined investment, innovation and the resilience of the EU protein sector.

The groups then called on the European Commission to develop a transparent, scientifically robust and coherent framework that supports both climate and energy objectives and sustainable European protein production.

Statement signatories were:

- COCERAL, the European Association of trade in cereals, oilseeds, rice, pulses, olive oil, oils and fats, animal feed and agrosupply;

- COPA-COGECA, European farmers and European agri-cooperatives;

- Donau Soja, the European, multi-stakeholder, not-for profit supporting the European protein transition;

- ...

According to the European Commission, in the 2025/26 marketing year, the EU increased its exports of common wheat by 8% compared to the previous season, from 21.62 to 23.42 million tonnes, most of which were delivered to Nigeria and Morocco. The main exporters were Romania (7.29 million tonnes), France (5.56 million tonnes), Poland (3.28 million tonnes), Germany (2.34 million tonnes) and Lithuania (2.28 million tonnes).

Barley exports increased by 72% compared to the previous season to 8.98 million tons, of which 1.9 million tons were delivered to Saudi Arabia and 1.7 million tons to China.

Corn imports in the 2025/26 MY decreased by 7% to 18.47 million tons, in particular, supplies from Ukraine - from 11 to 8.5 million tons (46% of imports), while supplies from the USA increased from 4 to 5.9 million tons (31.9%), and from Brazil - from 1.6 to 3 million tons (16.3%).

Rapeseed imports decreased by 29% to 5.4 million tons, in particular from Australia - from 3.6 to 2.14 million tons (39.7% of supplies), from Ukraine - from 2.41 to 1.597 million tons (29.6%), from Canada - from 1.13 to 0.87 million tons (16.2%), while supplies from Moldova increased from 105 to 274.8 thousand tons.

Soybean imports decreased by 3% to 14.1 million tons, in particular from Brazil - from 5.9 to 4.4 million tons (31.3% of supplies), from Ukraine - from 1.58 to 1.3 million tons (9.5%), while supplies from the USA increased from 6.3 to 7.28 million tons (51.7%).

Despite the decrease in the sunflower harvest, in the 2025/26 MY the EU increased its exports by 72% to 988.5 thousand tons, of which 720 thousand tons were shipped from Romania and 216 thousand tons from Bulgaria, in particular 794 thousand tons were delivered to Turkey. At the same time, sunflower imports increased by 99% to 1.21 million tons, in particular 670 thousand tons were delivered from Argentina, 335 thousand tons from Moldova, of which 565 thousand tons were purchased by Bulgaria and 248 thousand tons by Romania.

Imports of soybean meal decreased by 1% to 19.2 million tons, and palm oil by 4% to 2.9 million tons.

At the same time, the European Commission notes that the data provided is incomplete, as it does not take into account information for France starting from 2024, for Bulgaria and Ireland starting from July 2023, and for Greece starting from January 2026.

A batch of soybean oil supplied by Taichung-based Central Union Oil was found to contain excessive levels of benzo[a]pyrene, a carcinogenic compound.

TAIPEI: Taiwan on Wednesday (Jul 8) widened a precautionary recall of food products linked to contaminated soybean oil, with more than 400 items, including packaged meals and instant noodles, now reportedly ordered to be pulled from shelves.

The expanding food safety scare has also triggered a political row, with opposition lawmakers accusing the government of mishandling the response and calling for the health minister and other senior officials to resign.

The case came to light on Jul 1 after the Taiwan Food and Drug Administration (TFDA) said Taichung-based edible oil supplier Central Union Oil had detected excessive levels of benzo[a]pyrene in a batch of “soybean salad oil”.

Benzo[a]pyrene is classified as carcinogenic to humans by the International Agency for Research on Cancer. It is a type of polycyclic aromatic hydrocarbon, which is formed during the incomplete burning of organic materials such as coal, oil, tobacco and wood.

About 1,300 metric tonnes of the affected oil had been found to contain 8.1 micrograms per kg of benzo[a]pyrene, more than four times Taiwan's legal limit of 2 micrograms per kg.

The affected oil was distributed to three food manufacturers - Tai Sun Enterprise, Fwusow Industry and Formosa Oilseed Processing. It was shipped between Apr 8 and 10, a TFDA official said on Wednesday.

The recall has expanded in stages. An initial recall was launched on Jul 1, targeting the problem oil and the products made by the three companies.

On Jul 4, this was expanded to further downstream products containing at least 20 per cent of the affected oil. This was widened on Jul 7 to cover all downstream products made with the affected oil, regardless of the proportion used.

The list of recalled products released by the TFDA comprised 401 items as of Wednesday, local media reported. It includes salad dressings, seasoning sauces, bakery fillings, ready-to-eat food, as well as flavoured sauces.

As we predicted, the low supply of sunflower in Ukraine at the end of the season led to the shutdown of some plants, while those enterprises that have the ability to process rapeseed are beginning preparations for its acceptance, which reduces demand for sunflower and, accordingly, affects prices.

During the week, purchase prices for sunflower in Ukraine sharply decreased by 500-1000 UAH/t to 32,000-33,000 UAH/t (oil content 50%) with delivery to the factory.

Export demand prices for sunflower oil remain at a high level of $1,330-1,345/t delivered to ports, while supply prices for Ukrainian sunflower oil have increased to $1,370-1,385/t FOB and significantly exceed prices for Russian sunflower oil (which is $1,300/t FOB) and Argentinean sunflower oil ($1,270-1,300/t FOB).

Favorable weather with low temperatures and precipitation forecast for the coming days in Ukraine and the Russian Federation are improving the potential of the sunflower harvest, which is putting pressure on the prices of the new harvest and reducing demand for supplies of sunflower oil from the old harvest.

In the EU, a heat wave is reducing the potential yield of spring crops, but the forecast for sunflower production remains at 9.6-10.2 million tons, which will exceed the previous season's figure by 1.2-1.7 million tons due to an increase in sowing areas.

Pakistan's edible oil and oilseed import bill continued its upward trajectory during the first 11 months (July–May) of FY2025–26, rising by 11.1% year-on-year to US$5.522 billion, compared with US$4.971 billion in the corresponding period of FY2024–25, according to the official data available with Wealth Pakistan.

The import bill had already recorded a significant increase in the previous year, climbing from US$4.190 billion in FY2023–24 to US$4.971 billion in FY2024–25, reflecting an annual growth of 18.6%.

Rising domestic demand is expected to push the country's edible oil and oilseed import bill to US$6 billion by the end of the fiscal year 2025-26.

Palm oil continued to dominate Pakistan's edible oil imports. Palm oil imports stood at 3.279 million tons during July-May 2025-26, compared with 3.213 million tons a year earlier and 2.997 million tons in 2023-24.

Soybean oil imports, however, declined to 0.098 million tons from 0.321 million tons last year, while imports under other edible oils edged down to 0.090 million tons from 0.093 million tons in 2024-25. Overall, edible oil imports during the period amounted to 3.457 million tons.

At the same time, the country increased oil extraction from imported oilseeds, reflecting higher crushing activity. Total edible oil extracted from imported oilseeds reached 0.848 million tons during the fiscal year 2025-26, compared with 0.542 million tons in 2024-25 and 0.597 million tons in 2023-24. This was achieved by crushing an estimated 3.693 million tons of imported oilseeds, up from 2.163 million tons last year.